Most employees aren't thinking about their 401(k) when they sit down at their desk. They're thinking about last month's credit card bill, whether they can cover a surprise car repair, or how far behind they've fallen on their financial goals.

That anxiety doesn't clock out when the workday starts, and the cost to employers is staggering. Financial stress is estimated to cost U.S. businesses $183 billion annually in lost productivity alone. It shows up in absenteeism, employees distracted at work, and healthcare claims that didn't have to happen.

A strong financial wellness program and a genuine commitment to employee financial wellness is one of the highest-leverage investments HR and benefits leaders can make. The good news is that benefits leaders are better positioned than anyone to do something about it.

What Is a Financial Wellness Program?

A financial wellness program is an employer-driven initiative designed to improve employees' financial stability and reduce stress through education, tools, and personalized support.

The best programs address the full range of where employees actually struggle, not just in retirement planning, but also the near-term pressures that consume most people's financial energy day to day.

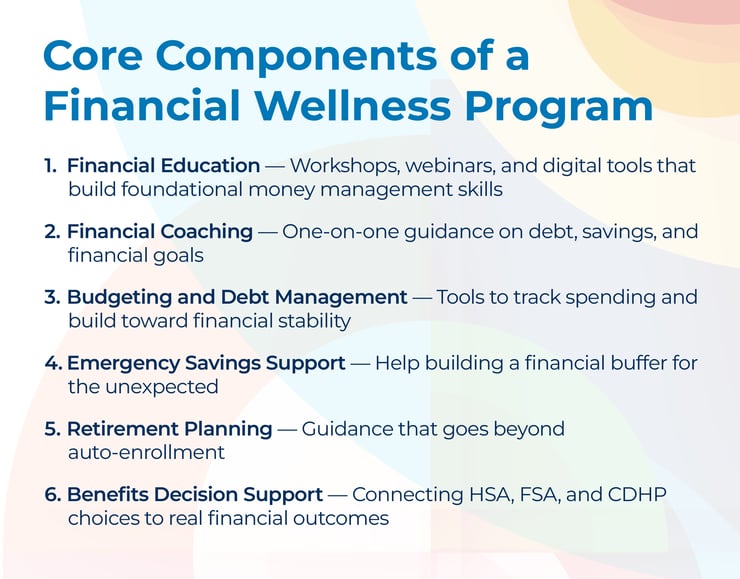

Core components of an effective financial wellness program include:

- Financial education and financial literacy resources — workshops, webinars, and digital tools that build foundational money management skills

- Financial coaching or counseling — one-on-one access to experts for personalized guidance on debt, savings, and financial goals

- Budgeting and debt management resources — tools that help employees track spending and work toward specific financial goals

- Emergency savings support — programs that help employees build a financial buffer for unexpected expenses

- Retirement and long-term savings planning — guidance that goes beyond auto-enrollment and helps employees understand what they're actually building

- Health benefits decision support — guidance on Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), and Consumer-Directed Health Plans (CDHPs) that connects benefits selection to financial outcomes

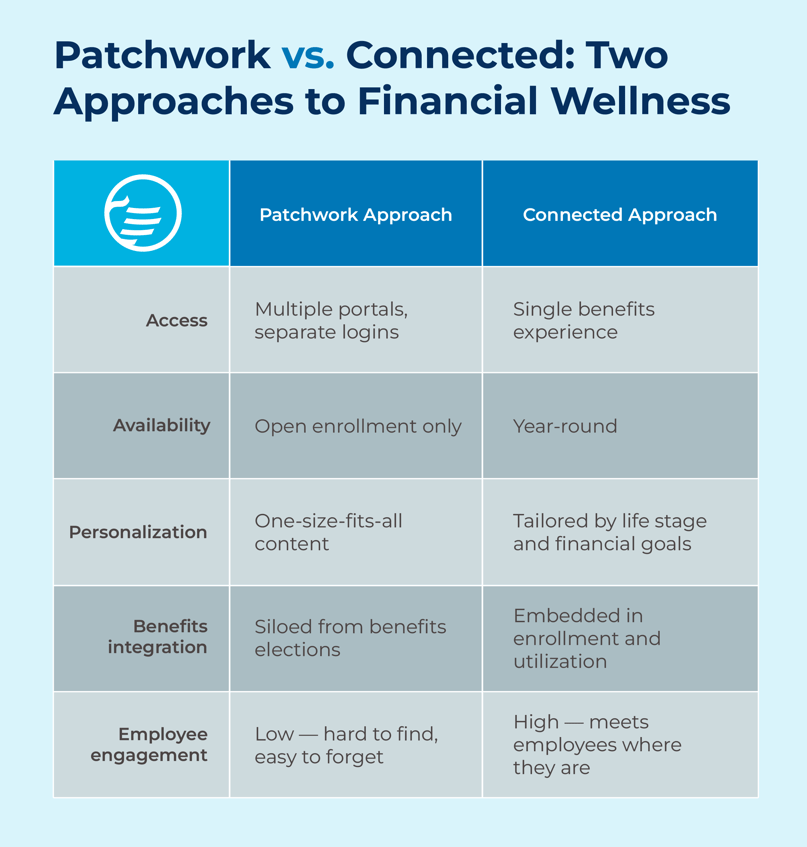

A collection of standalone tools and vendor portals isn't a program, though. The employers seeing real results are the ones embedding financial wellness into a single, connected benefits experience that employees can actually navigate.

Why Financial Stress Is an Employer Problem, Not Just an Employee One

It's tempting to think of financial wellness as a personal matter, or something employees should sort out on their own time. The data says it should be a concern of employers as well.

A 2025 Bank of America analysis of nearly 89,000 401(k) participants found that 66% of employees are stressed about their financial situation and 76% believe the cost of living is outpacing their income growth. This isn't a fringe issue. It's the majority of your workforce walking in every morning carrying real financial anxiety and in many cases, very real financial issues they don't know how to address.

The Productivity Cost

Financial stress doesn't stay home. Research estimates that affected employees lose 7 to 8 hours of productivity per week due to financial distraction. Data from PwC shows that addressing employee financial health can lead to a 40% improvement in productivity and a 23% reduction in absenteeism. The ROI math isn't complicated.

The Healthcare Connection

There's a less obvious cost that HR and benefits leaders often miss. Financial stress drives unhealthy behaviors like deferred care, skipped prescriptions, and ignored preventive screenings, all of which eventually show up as higher claims costs.

Research has also drawn strong links between personal financial strain and mental health challenges, creating a compounding effect that touches every dimension of employee well-being. Most don't connect their benefits decisions to their finances at all. That's a gap that benefits teams are uniquely positioned to close.

The Business Case for Investing Now

If your organization hasn't prioritized offering financial wellness benefits yet, you're increasingly in the minority. More than 70% of large employers now offer some form of financial wellness initiative, up from 59% the prior year. Adoption is accelerating fast, and for good reason.

Even with high adoption though, only 44% of employees feel completely supported in their financial wellness by their employer.

For organizations willing to close that gap, the differentiation in recruiting and retention is real. Majorities of Gen Z and millennial employees now expect their employer to actively support their financial wellness, making it a core part of the employment value proposition rather than a bonus perk.

How to Build a Financial Wellness Program That Works

Knowing you need a financial wellness program and knowing how to build one are two different problems. For HR and benefits leaders, here's where to focus.

Start with Employee Needs, Not Vendor Catalogs

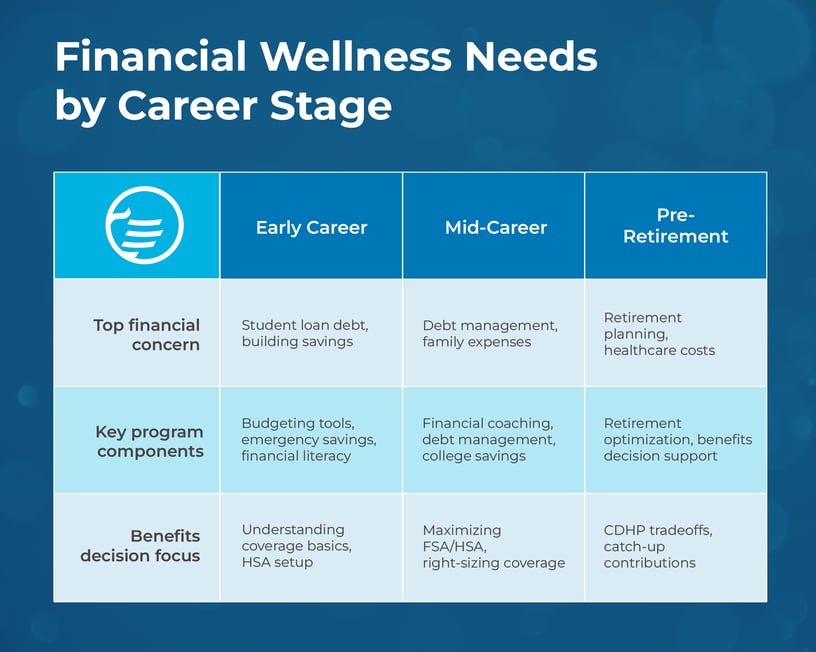

The most common mistake is starting with a solution rather than a diagnosis. Before selecting vendors or designing curriculum, survey your workforce to understand where the real pain points are.

Are employees dealing with student loan debt? Struggling to build emergency savings? Confused about their benefits options? The answers will vary by generation, life stage, and income level.

A 28-year-old managing student loan repayment has fundamentally different financial goals than a 52-year-old trying to maximize retirement contributions in the last decade of their career. A program that tries to serve everyone with the same content ends up serving no one particularly well. Make personalization a design principle from the start.

Make It Accessible and Year-Round

A one-time financial wellness workshop during open enrollment isn't a program. Real behavior change requires sustained, accessible resources that employees can return to as their personal financial circumstances evolve.

That means meeting employees where they are: mobile-first, easy to find, and available when they have a question in November just as easily as in October. The decision-support tools that work best are integrated into the benefits experience itself, not siloed in a separate portal that employees forget about two weeks after enrollment closes.

Connect Financial Wellness to Benefits Enrollment

This is where benefits teams have a significant and often underused advantage. Benefits decisions are financial decisions, every one of them.

Choosing between a high-deductible health plan and a PPO, deciding whether to contribute to an FSA, selecting the right level of life insurance coverage — these choices have real dollar consequences that most employees don't fully understand at the time they're making them.

Integrated benefits and expense management tools that help employees understand the cost implications of their coverage choices are one of the highest-leverage moves a benefits team can make. When employees understand how their benefits connect to their financial goals, engagement goes up and costly underutilization goes down.

Employer Checklist: Building or Auditing Your Financial Wellness Program

Whether you're building from scratch or taking stock of what you already have, this checklist gives you a practical framework to evaluate where you stand. Use it as a starting point for your next benefits strategy conversation.

Assess

-

Have you surveyed employee financial stress levels and identified your workforce's top pain points (debt, savings gaps, healthcare cost confusion)?

-

Do you know which employee segments are most financially vulnerable, and how needs differ across generations and income levels?

Design

- Does your program address near-term financial needs (emergency savings, debt management) alongside long-term financial goals (retirement, wealth building)?

- Is it personalized by life stage and demographic, rather than delivering the same content to everyone?

Integrate

- Is financial wellness embedded in your benefits experience, or does it live in a separate portal employees have to seek out?

- Can employees access financial guidance and tools during open enrollment and throughout the rest of the year?

Communicate

-

Do employees know the program exists, where to find it, and how to use it?

-

Are you using multiple channels (mobile app, email, in-app notifications) to drive sustained awareness and engagement?

Measure

-

Are you tracking program participation rates, engagement trends, and downstream outcomes?

-

Have you established baselines for financial stress, absenteeism, and productivity so you can measure improvement over time?

If you're checking every box here with confidence, you're ahead of most organizations. If several are question marks, you have a clear starting point.

The Bigger Picture

Employee financial wellness programs have moved from a peripheral benefit to a core component of a well-designed total well-being strategy. The employers winning on this are building programs that meet employees where they are, connect financial guidance to the benefits decisions employees are already making, and sustain engagement year-round.

The employee expectations are real, the business outcomes are measurable, and the competitive stakes are rising. The question isn't whether financial wellness belongs in your benefits strategy. It's how quickly you can make it work.

Empyrean helps employers build benefits experiences that activate financial wellness alongside every other dimension of employee well-being, through personalized guidance, integrated decision support, and year-round engagement. If you're ready to see what that looks like for your organization, we'd be glad to show you.